Trading Excesses (Snail no. 2)

Why are we paying for trading activity that we don’t need?

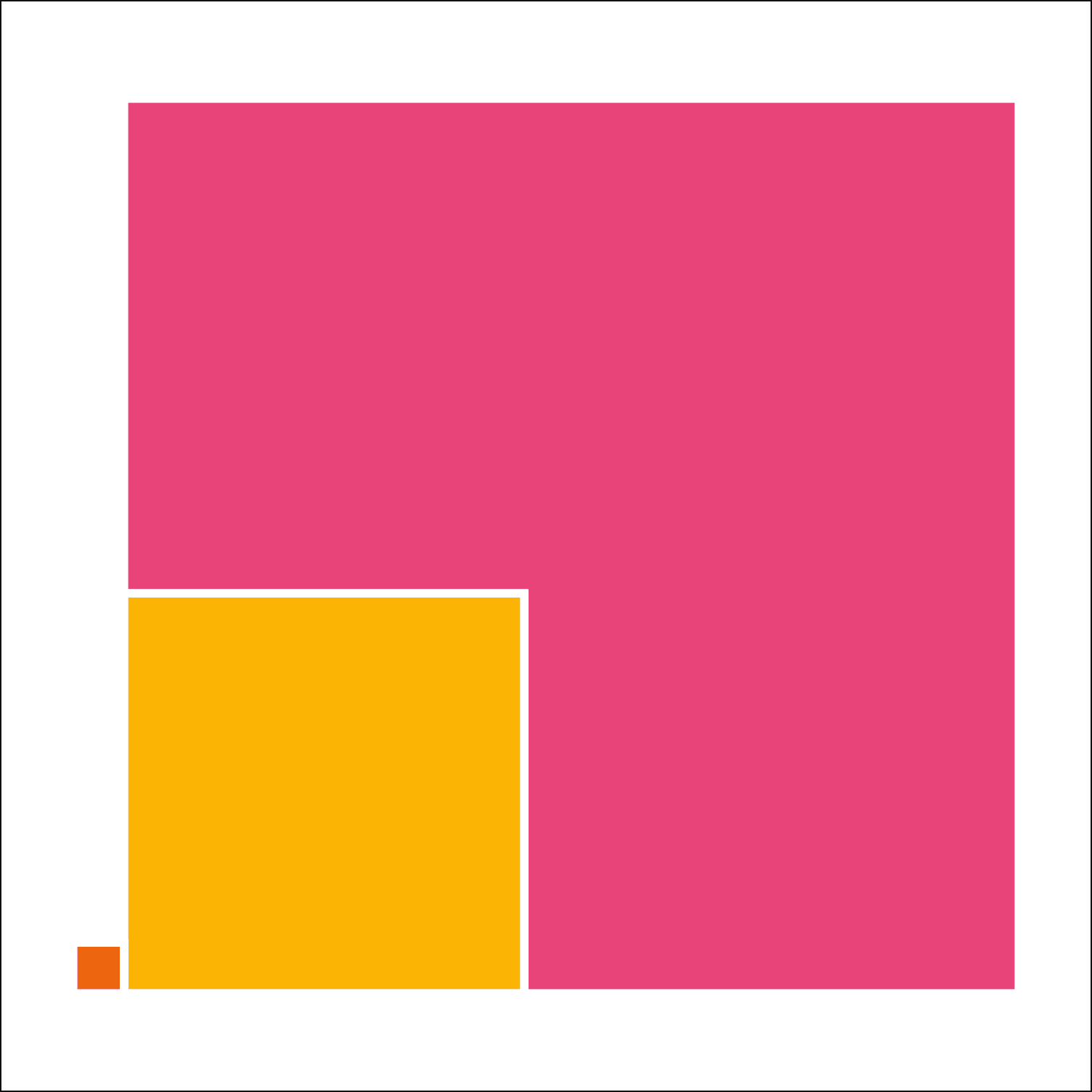

The head of the snail shows the requirement for foreign currency exchange to support UK imports and exports. The actual volume of sterling traded in London is shown in yellow. The total of all currencies traded in London is shown in pink.

Financial traders extract vast sums of money, but without creating anything new of value.

This image illustrates the daily trading in London’s foreign exchange markets. The little orange box that is the head of the snail is the actual amount of the UK’s imports and exports. So this is roughly the amount of exchange from pounds sterling to foreign currencies and vice versa that is needed to service that trade. In 2022 this was about £6 billion each working day.

The much larger yellow box, on the other hand, is the amount of exchange from pounds sterling to foreign currencies and vice versa that is actually taking place on the London market. This is in the region of £400-500 billion per day.

And the big pink box is the total amount of currency trading on the London market, most of which does not involve the pound sterling at all. This is in the region of £2,500 billion per day.

How useful is any of this? Why are people trading vast sums in excess of what is needed to manage actual trade?

The answer is - because they can. Although the activity produces nothing new or useful, there is a big opportunity here for traders to accumulate money simply by recording transactions. As in all markets, they buy as cheaply as they can, and they sell for the highest price possible. Their margins may be small in percentage terms, but the huge sums involved mean that the profits can be very substantial.

We are all paying for this. The money is flowing through the economy from our purchases into traders’ hands. Those profits make imported goods more expensive and put up the price of people’s holiday money, too. The speculative nature of the market encourages volatility as traders bet against the pound or some other currency, which creates costs for importers which they pass on to customers.

To make matters worse, the huge resources tied up in these and other financial markets are not available to be used in more productive ways. And it’s not only the money, which could be much better spent. All the skills of the clever people working in these markets are unavailable to the productive economy, where they could be adding real value.