Boardroom Excesses (Snail no. 1)

Are top bosses paid to do the wrong thing?

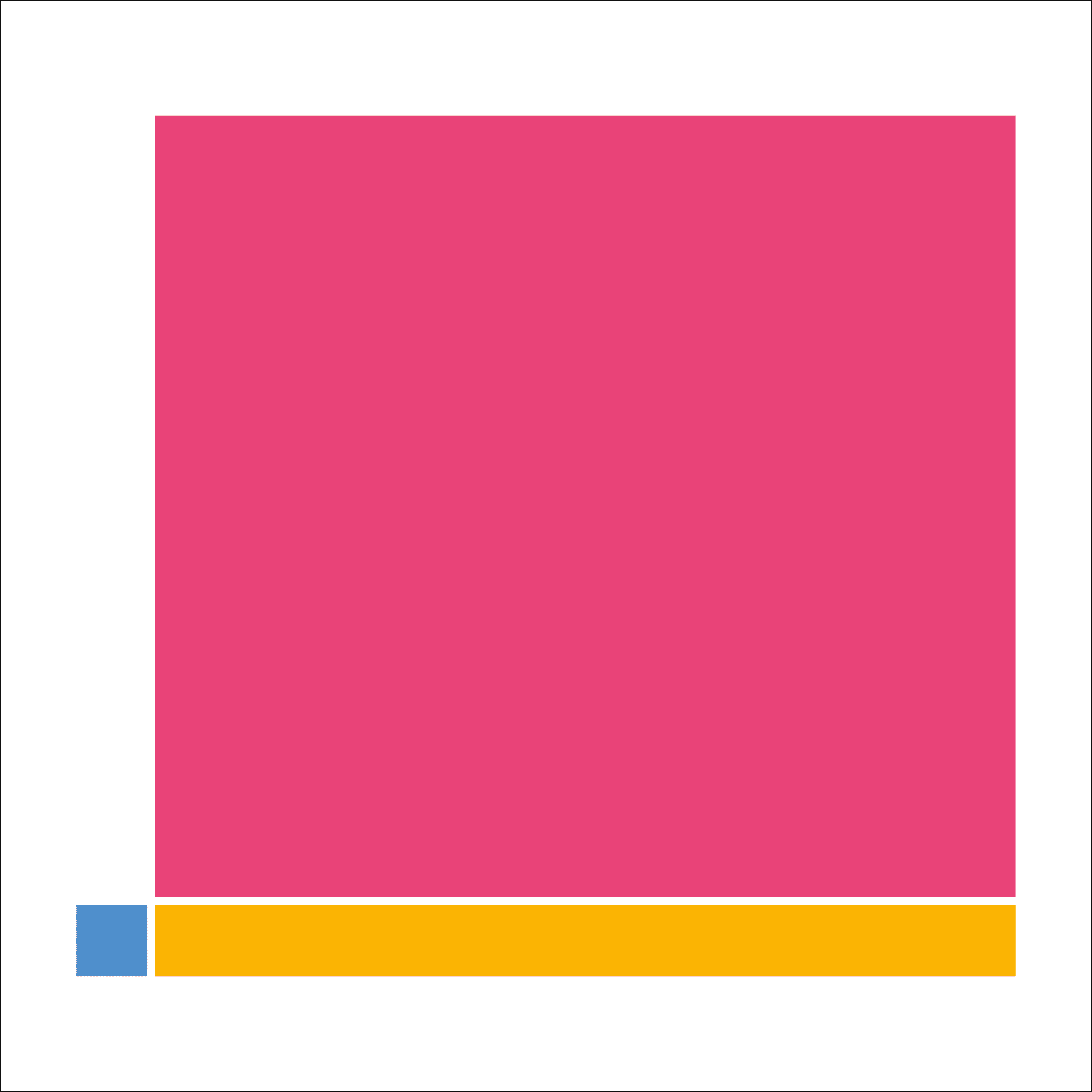

The head of the snail shows typical worker pay. This is compared with the pay of top chief executives in 1980 (yellow) and 2022 (pink).

The UK's top bosses are prioritising wealth accumulation over real wealth production.

This image shows the explosion in pay of the people in charge of the UK’s one hundred biggest companies compared with their workers in the last 40 years. Nearly a quarter of these are financial companies of one sort or another..

The small blue box - the head of the snail - represents the pay of a typical full time worker. The yellow box shows how much more than a worker those top bosses were paid on average in 1980 - about eleven times more. The big pink box shows the equivalent ratio for 2022, when the top one hundred bosses were paid 118 times more than their typical full time worker, an average of £3.91m each.

This story about excessive pay is not just about fairness or equality. If you take that £3.91m and spread it around a large workforce it won’t go very far. Much more important is the reason for the pay, which is justified not by the usefulness of a company’s productive activity but the delivery of “shareholder value.” That means an increase in the company’s share price and the amount of money it returns to investors through dividends and share buybacks.

Much of the money in that big pink box is a bonus of some sort, tied to how much money the company is able to extract from the rest of the economy to pass on to its shareholders. Often the main driver of these executive bonuses is not even the profitability of the business activity, but the performance of a company’s share price.

What the image reveals, therefore, is a not-so-subtle shift in the objectives of these top company bosses, who now prioritise wealth extraction over real production. Their main incentive is the amount of money value they can return to shareholders to meet their own, short term bonus targets. Reducing staff wages and benefits, increasing prices, and constructing complex, cross border financial arrangements to reduce taxes are all extractive processes that work much more quickly than long term investment in new talent, products and processes.