The family silver

The privatisation of the UK’s public utilities has caused a colossal transfer of money from ordinary families to the already-rich.

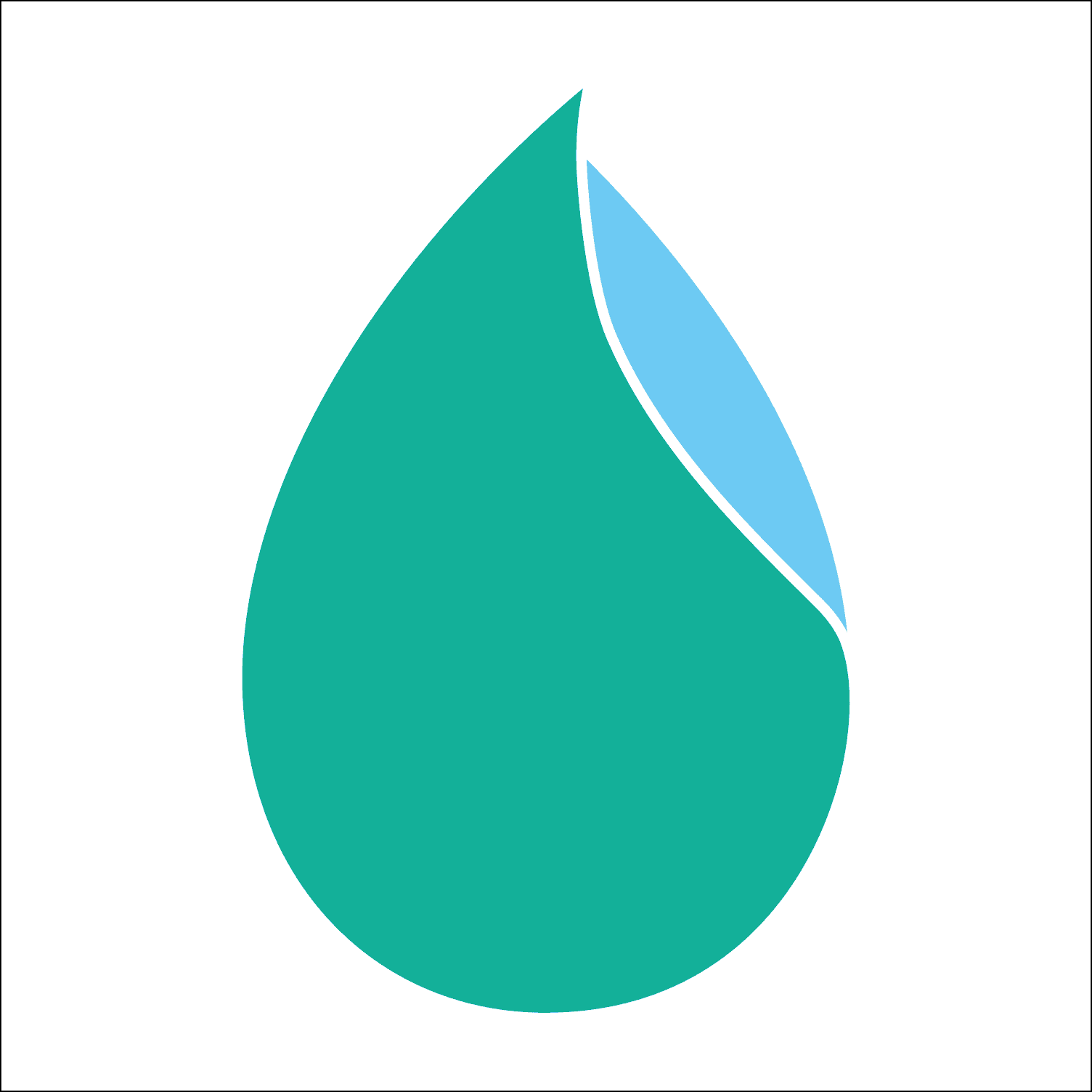

The blue area shows the sale proceeds when the UK water industry was privatised in 1989. The green area shows the dividends paid to the new owners between 1989 and 2019.

The government's fire-sale of the UK's public utilities in the 1980s and '90s has not worked out well. We are all paying the price.

In 1989, the state-owned regional water boards in England and Wales were packaged up into ten shareholder companies and the shares sold to private investors on the open market. The total raised, after expenses and debt write-offs, was about £6.5 billion. This is shown by the blue section of the image.

These companies proved highly profitable. Between their sale in 1989 and the year 2019 they are reported to have paid out £57 billion in dividends to investors - almost 9 times the amount the government received from the sale. This is shown by the green section of the image.

The same report shows that from 1991 to 2021 the water companies, which were debt-free at privatisation, took on debt of £52 billion - almost the amount they have paid out in dividends. The cost of servicing that debt has been calculated at about 20% of customers’ bills. Meanwhile, between 1991 and 2018 they invested £123 billion of bill payers’ money in the water and sewage systems.

If these huge numbers might make one's head spin, that is precisely the intention. There is no wish to provide clarity. One thing is clear, however: the object of the managers of large private companies is to extract as much money as possible for shareholders, with the interests of employees, customers and the environment subservient to that. The law and the regulators may require certain standards, but their capacity (and willingness) to enforce them is limited, as persistent leaks, sewage spills and other scandals show.